May 2021 Global Capacity Growth Analysis

By Kieran Clark

By Kieran Clark

By Kieran Clark

By Kieran ClarkMay 21, 2021

Bandwidth demand continues to explode as both businesses and consumers increasingly rely on cloud services – especially in the post-COVID world. Hyperscalers continue to increase their percentage of overall telecommunications traffic and are driving more and more cables to meet their own demands. New markets are connecting to the global telecommunications network and continued desire for alternate routes to provide route diversity is keeping new system activity relatively high.

All of this adds up to a huge need for the submarine fiber industry to stay ahead of the curve and continue to provide additional capacity to meet these growing needs. Can we keep up the pace?

Welcome to SubTel Forum’s annual Subsea Capacity issue. Every May, we aim to take the industry’s pulse by looking at the future of our section of the telecoms market. Specifically, how much cable owners are planning to add to the ever-growing pool of capacity and what technologies are being implemented. The data used in this article is obtained from the public domain and is tracked by the ever-evolving SubTel Forum Submarine Cable Database, where products like the Almanac, Cable Map, Online Cable Map and Industry Report find their roots.

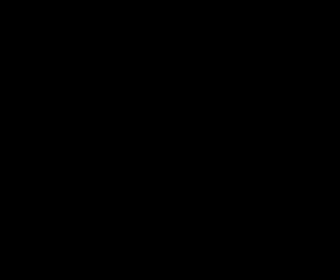

Figure 1: Global System Capacity by Year, 2016-2020

As new systems come into service and existing systems are upgraded, there is a continuing upward trend in global capacity to address the world’s demand for more telecoms services. This is mostly due to an ever-increasing demand for low latency, high bandwidth international connections, and to the almost exponential increase in demand for mobile and cloud services observed over the last few years. These factors show little signs of slowing down, so there is a strong expectation that demand will continue to rise at a rapid pace in the coming years.

The overall Compound Annual Growth Rate (CAGR) for the period 2016-2020 was 10.3 percent. Capacity increased the most by a CAGR of 13.8 percent and 14.2 percent during the years 2017 and 2018, respectively. There were only 9 systems that entered service in 2018 compared to the 15 in 2017 yet a similar capacity increase was observed. (Figure 1) With easy and cheap access to 100G wavelength upgrades and 200G/400G beginning to enter regular service, this comes as little surprise. New technology such as C+L band and Space Division Multiplexing (SDM) alongside an increase in fiber pair counts has also contributed to this capacity increase – despite the lower number of new cables.

To continue reading the rest of this article, please read it in Issue 118 of the SubTel Forum Magazine on page 8 or you can find it here on our archive site here.

news via inbox

Sign up to get the latest updates straight to your inbox!